It may take a few weeks to process a gap insurance claim, but this depends on the specifics of the accident or theft that led you to file the claim. Your vehicle insurance company must first determine the actual cash value of your vehicle. Your gap insurance provider will then verify your loan or lease details before your gap coverage pays out.

Read the editorial guidelines for Progressive Answers auto to learn why you can trust the information here about car insurance.

Gap Insurance Didn’t Pay Off My Loan Balance – Here’s Why

Having your car declared a total loss can be extremely stressful To make matters worse, you may still owe money on your auto loan after your insurance company issues the settlement. This is precisely the kind of situation gap insurance is designed to handle So why didn’t your gap policy pay the full remaining balance after your car was totaled?

There are a few common reasons why gap insurance might not pay out the full amount you expected Understanding these scenarios can help you avoid surprises and ensure you receive all the benefits you’re entitled to

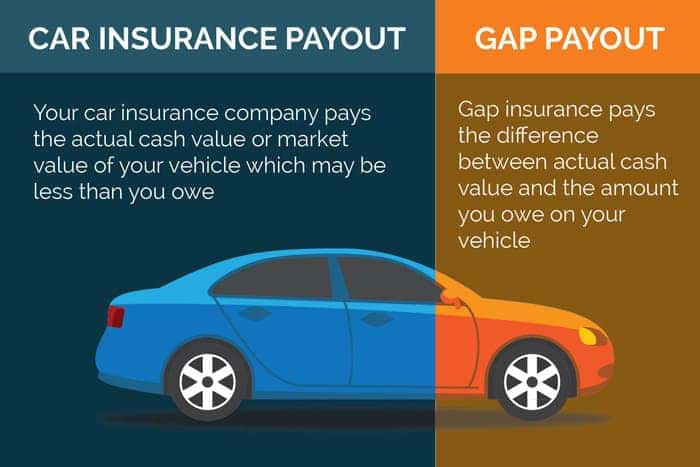

What is Gap Insurance?

Let’s start with a quick refresher on how gap coverage works. Gap insurance protects you when you owe more on your auto loan than your vehicle’s actual cash value (ACV).

For example:

- You owe $15,000 still on your car loan

- Your car is totaled in an accident

- Your insurance company declares it a total loss and pays a $10,000 ACV settlement

- This leaves you with a $5,000 balance still owed to the lender even though you no longer have the vehicle

Gap insurance pays this leftover “gap” amount to the lender so you don’t end up continuing to pay a loan for a non-existent car.

However, sometimes gap insurance doesn’t pay the full remaining balance as expected. Here are the most common reasons for reduced or denied gap claims:

- You Were Behind on Loan Payments

One of the most frequent reasons for a lower gap payout is if you were behind on your monthly car loan payments when the vehicle was totaled. Gap policies require that you be up-to-date on your loan payments at the time of loss to receive full benefits. Otherwise, the insurer will deduct missed payments from the payout.

For example:

- You owe $15,000 still on the loan

- You’re 3 months behind on payments, so $1,500 is past due

- The insurer deducts the $1,500 arrears from the $15,000 balance

- Gap pays only $13,500 of the remaining loan balance

Always bring your loan current if you’ve fallen behind to maximize your gap claim if your car is totaled.

- Inaccurate Loan Payoff Quote

Gap insurers rely on getting an accurate final loan payoff quote from the lender to calculate the correct benefit amount. If the lender provides an inflated amount, you may not get the full payout you’re entitled to.

For example, the lender may include:

- Late fees that should’ve been waived

- Excess interest charges

- Fees for canceled add-on products like extended warranties

To avoid this when filing a gap claim:

- Review the loan payoff quote provided to the insurer

- Dispute any incorrect charges

- Ask the lender to generate an updated payoff quote

This ensures the gap calculation uses the right loan balance amount.

- Excess Mileage Penalties for Leased Vehicles

If you leased the vehicle, excess mileage penalties can lead to lower gap payouts. Most lease contracts strictly limit annual mileage. Exceeding that limit when the car is totaled means the leasing company may charge off-lease mileage fees.

Gap insurance won’t cover these excess mileage penalties. The insurer will deduct the charges from the remaining lease payoff amount when calculating the benefit.

- Exclusions for Certain Loan Types

Some types of car loans may be excluded from full gap coverage. For example, policies often limit benefits for:

- Balloon payment loans – You may not get gap coverage for large final “balloon” payments.

- Loan extensions – Extended loan terms may not be eligible for gap benefits.

- Refinanced loans – Refinancing into a second loan can invalidate gap coverage from the first loan. Always re-purchase gap if you refinance.

- Deductible Reimbursement Limits

Most gap policies include some reimbursement for your auto insurance deductible if it’s not waived in the claim settlement. However, coverage is usually limited to around $1,000.

For example, if you choose a $2,500 deductible and your insurer doesn’t waive it after a total loss, gap would only pay $1,000 of that amount. The rest is out of your pocket.

- Exclusions for Customized Vehicles

If you make aftermarket modifications and upgrades, they may not be covered by gap policies. For example, adding:

- A turbocharger

- Premium sound system

- Expensive rims

- Custom paint job

Gap insurers will only pay to cancel the remaining loan balance based on the vehicle’s original factory configuration. Any customization costs won’t be included in the gap benefit calculation.

- Reduced Payouts from Vehicle Wear & Use

Insurers factor in reductions for normal wear and tear when determining ACV settlement amounts after a total loss. For example, higher mileage cars may get less.

But the original full loan balance doesn’t change to account for depreciation over time from driving. This growing difference reduces the “gap” the policy covers.

While gap insurance can provide valuable protection, it doesn’t completely eliminate risks in every total loss situation. Understanding exclusions protects you from surprises if you need to file a gap claim.

What to Do if Gap Won’t Pay the Full Amount

If your gap insurer denies paying any part of your remaining loan balance after a total loss, you have options to fight for the benefits you deserve:

-

File an appeal – Formally dispute the results and request a review. Provide documentation to support your argument for the full amount under your policy.

-

File a complaint – Reach out to your State Department of Insurance if you feel the insurer is acting in bad faith. The regulators can investigate on your behalf.

-

Seek legal representation – An insurance attorney can review your case and determine if grounds exist to compel the gap company to pay through legal action.

-

Negotiate a settlement – Even if the law is on the insurer’s side, a negotiated compromise agreement can sometimes be reached. This may at least help defray some costs the reduced gap benefit leaves you with.

With persistence and support, you may successfully appeal a denied gap insurance claim. But it’s best to understand potential limitations upfront before purchasing coverage.

Making the Most of Gap Insurance Protection

While gap coverage has some catches, it remains an important product for many car buyers. To maximize protection:

✔️ Review your policy to understand exclusions

✔️ Keep loan payments current at all times

✔️ Avoid excessive mileage if leasing

✔️ Don’t extensively customize vehicles after purchase

✔️ Confirm accurate loan payoff amounts are used

✔️ Re-purchase gap if you refinance your loan

✔️ Only make covered repairs prior to a total loss claim

✔️ Keep records validating your loan and lease history

Gap insurance can provide vital protection after a total loss. Taking the right steps ensures no surprises stop your policy from paying as expected.

Frequently Asked Questions

Understanding why gap claims sometimes fall short requires answering some common questions about how the policies work:

How does gap insurance calculate payout amounts?

The gap benefit is based on the difference between your loan/lease payoff amount and your auto insurance ACV settlement. The original financing amount is reduced by factors like missed payments and exclusions to reach the final payout.

Can you negotiate a higher settlement with the gap insurer?

You can try negotiating, but most insurers strictly follow the policy terms and total loss valuations. Partial payment negotiations may be possible in special cases through legal representation.

What if the auto insurer undervalued my totaled car?

You can dispute the settlement amount with your auto insurer. Provide evidence like dealer prices on comparable vehicles. If they revise the value up, your gap claim will be recalculated accordingly.

Will gap insurance still pay if I was uninsured when my car was totaled?

Most policies allow gap claims without auto insurance. The vehicle’s value will be determined from third-party valuation sources instead of an insurer’s settlement amount.

Can I get a refund after my gap claim falls short?

Unfortunately, you can’t cancel and get a refund after making a gap claim, even if benefits fall short. However, you can cancel unused coverage prior to making a claim and get a prorated refund.

Gap insurance can provide valuable financial protection after a total loss. But it’s essential to understand potential limitations and exclusions. Taking the right steps ensures your policy pays as expected if you ever need to file a claim.

How do you file a gap insurance claim?

There are different ways to file a gap insurance claim, such as in person, over the phone, or online. You will get the money you owe your lienholder if your comprehensive or collision coverage claim is approved after your car is stolen or totaled. This is because of your gap insurance policy.

You can get help from your car insurance company or gap insurance provider if you have questions or don’t know what to do. Most of the time, you can keep track of the gap insurance claims process once you’ve filed your car insurance claim.

Pro tip:

Progressive offers loan/lease payoff coverage in most states. This is like gap insurance coverage, but there are a few important differences. One big difference is that loan/lease payoff coverage only pays out up to a certain percentage of your car’s value. The exact percentage varies by state. Loan or lease payoff also doesn’t cover any extra fees that come with a loan or lease, like finance charges or charges for driving over the mileage limit.

When does gap insurance not pay?

This type of insurance is only meant to protect you if you owe more on your loan or lease than the car is worth. When that happens, the money you get from the insurance company isn’t enough to pay off your loan or lease. Gap insurance wont pay for:

- Injuries

- Repairs to your vehicle

- A new car

- Damage to someone elses vehicle

- Negative equity you rolled over from a previous loan

- Cost of optional products such as vehicle service contracts

Extra fees related to your loan or lease, like fees for going over your mileage limit, might not be covered either. Keep in mind that your gap insurance won’t pay out if you don’t owe more than the car is worth.

Gap Insurance Did Not Pay Balance-A Must Watch

FAQ

Does gap insurance pay off a loan?

Can gap insurance be refunded?

Why won’t my gap insurance cover my car?

Why is my gap claim taking so long?